People have messaged me multiple times asking for my recommendation for a great course in economics. Hands down, your best option for learning economics, political theory, American History, and World History is Tom Woods’ Liberty Classroom.

Due to my current work situation, I am unable to continue writing weekly articles critiquing the latest Crash Course Economics video.

Fortunately, Crash Course Economics itself said that they were finished with “textbook economics” weeks ago, and the episodes are now delving into more sociological/behavioral economics subjects, which relate to economics, and are probably worthy of criticism in their own right. But since we’ve covered the basic economics principles already, and economics is just following those principles to their logical conclusions, I think the Crash Course Criticism readers are very well-equipped to analyze the Crash Course videos on their own.

The purpose of this blog is to analyze how Crash Course explains economics to their very large audience of mostly young people. I think we did a good job of that; we took Crash Course’s own arguments to their logical conclusions and showed what kind of predispositions to the different schools of economic thought that the Crash Course writers showed in their work.

Thank you to all of you who read, commented, or wrote me personally. It’s been a blast keeping this blog running, and I’m glad you could join in on the fun. If you’d like to stay informed on what my next project is, please sign up for the newsletter at http://www.crashcoursecriticism.com/newsletter/

We have entered a new phase of Crash Course Economics and Crash Course Criticism. Episode 30 marks the first episode without one of our co-hosts, Mr. Clifford. If you recall, Mr. Clifford was a co-host most dedicated to “textbook economics,” while the other co-host, Adriene Hill, was more focused on practical application and real world examples of economics in action.

Last week in the episode 29, the hosts announced that it was “the end of their textbook economics episodes,” which means that now we are going to get involved with subjects only tangentially related to economics. Let’s see how the first one turned out:

After watching the first episode, it appears that this new phase of Crash Course Economics will deal more with the “how-to” of being an adult, and preparing the audience with some of the most challenging subjects of life. Despite still being called “Crash Course Economics,” there’s not much economics in this episode, but let’s do what we can.

Income vs. Age

In 2010, an upper income man in the US was expected to live to age 89. The same lower income man would live to 76. And this shortened lifespan has a big economic impact.

In effect, the rich receive a lot more government benefits over the course of their lives. That 89 year old upper-income man would collect an average of $522,000 dollars in government benefits during his life, while the lower-income man would only collect an average of $391,000 dollars.

This wouldn’t be a Crash Course episode without left-leaning commentary and unexplained statistics. Following this part of the episode, Crash Course moves to a completely new subject without tying these statistics together or explaining them, so we’ll try to do that here.

Disclaimer: I could not corroborate these numbers from my research. I tried to find where Crash Course got these figures, but I could not find them through Google, and they do not list them in the video description, so I’m just going to accept them as fact.

If rich people live longer, then they have more of an opportunity to reap the benefits of Social Security and Medicare, which generally start paying out in your 60’s. The longer you can stay alive past your mid-60’s, the more time you will have to receive a check every month from Social Security, and the more opportunities you will have to get health care, which is covered by Medicare.

It appears that the rich receive more in government benefits over the course of their lives because they live longer. If left at that, the viewer is to the think “What a rip off! The rich live longer and they take more from the government? After they complain so much about the poor taking so much in welfare?! The rich are the real welfare recipients!”

What’s not mentioned in this episode is a comparison to how much the rich contribute to taxes over the course of their lives. With this in mind, it no longer appears that the rich get the most out of these government programs, considering they pay much more than they receive. The lower income level of Americans, while they receive less in total benefits, likely contribute much less than they receive.

Old Age and the Economy

So how do our on average longer lives affect the economy? Well, economic thought about this stuff varies. Some economists argue that increased lifespans are, in a very basic sense, good for the economy. When people live longer, they have more years to consume stuff, contributing to economic growth. On the other hand, long life tends to come with more health problems, and memory-related illnesses have become much more prevalent[…]

Note: This is a very strange non sequitur. If the question was about how long lives affect the economy, why does Crash Course start talking about the personal struggles of growing older? What does this have to do with the economy in general?

Economically-speaking, the part in bold above shows a clear bias towards the Keynesian (or any spending-centric) Economic School of Thought. We talk about this a lot on Crash Course Criticism, so I won’t go into it again, but Spending (as opposed to Saving) does not necessarily benefit the economy.

But if it did, shouldn’t Crash Course say what a great benefit it is to the economy that the United States health care system is so expensive? That money would otherwise be stagnant in some old person’s bank account, but now it’s being spent!

However, it could still be argued that longer lives could improve the economy in a different way. With people living longer, each person would have more time to produce things for the economy, whether its by retiring at a later age or by taking up a new interest in retirement. In either scenario, stuff would get produced where it otherwise would not have happened.

Conclusion

This week’s post is on the short side, since (ironically) Crash Course Economics does not give a lot for an economist to analyze. The episode in general, however, seemed like a great opportunity to have the mostly young audience of Crash Course start thinking about a serious challenge in life, and despite the economic lacking and obvious political bias, the episode seemed to have very good message: plan for your own death. It’s a hard subject to think about, especially for Crash Course’s target audience, but doing it will save your family a lot of trouble.

This week’s episode on Crash Course Economics deals with the United States Healthcare System. The episode didn’t really have much economics in it; it was more a series of fun facts about health care numbers.

It’s a shame because the US Healthcare System is a perfect subject to talk about how public policy and economics have responded to one another in the past 60 years or so. What an opportunity here for Crash Course! Unfortunately, Crash Course did not take advantage of these great examples, but we will here on Crash Course Criticism. Let’s do it:

United States Healthcare Assumptions

When talking about the US Healthcare System, Crash Course assumed a lot of things about the US system simply exist and have always existed, offering no explanation for how these phenomena came about or how economics could explain them. Let’s look at them now.

People Use Healthcare Insurance, and it’s Usually Paid by Your Employer

Insurance in general has been around for thousands of years, but it’s only recently that health insurance has been common. The first modern health insurance plan in the United States emerged in the 1930’s, but few used it. Until the 1940’s, people would pay doctor and hospital expenses out of pocket, and patients wouldn’t go bankrupt because of it.

During World War II, the government restricted employers from increasing the pay of their employees. As a natural economic reaction to get around these rules, employers instead would offer employees more benefits, including health insurance. This soon became the standard, and today many employers pay for their employees’ health insurance.

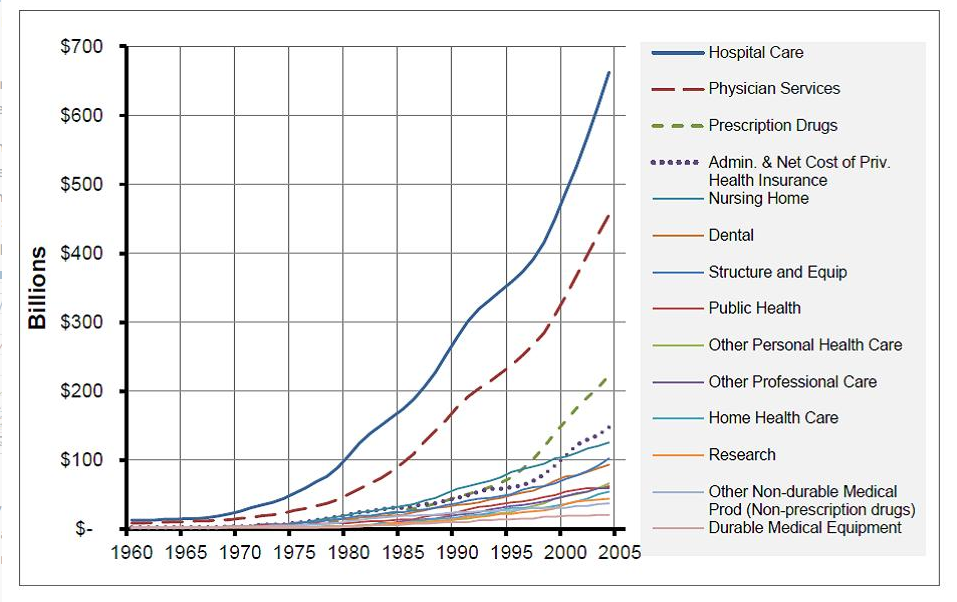

Healthcare Costs are Expensive

This was not always the case. Take a look at this graph:

As any media pundit will tell you, health care costs in the United States have exploded in recent decades, but the initial rise started in late 1960’s. What would make healthcare providers charge more for their services?

Medicare and Medicaid were both introduced in the mid-60’s, and Crash Course may have alluded to how this increases health care costs:

This is because the US doesn’t have a unified system that can aggressively negotiate with doctors, pharmaceutical companies, and other providers. They point out that Medicare and Medicaid often get a significant discount compared to small insurers.

In other words, Medicare and Medicaid do get a discount from providers, while normal insurers do not.

In another natural economic reaction, healthcare providers have to increase the price to normal insurers to cover the cost of providing the care at a discount rate to Medicare and Medicaid.

Economists might point to other restriction in the supply of healthcare, from the restrictions on the number of medical schools in the country to the restriction of hospital development through the Certificate of Need requirements.

Crash Course Gets it Right

On the other hand, Crash Course does recognize some major factors toward the increase in healthcare costs:

So why does the US spend so much more than other countries? Well, some argue that it’s due to high quantity of care per person. Since insurance companies, rather than patients pay providers, patients might want more care, like tests, procedures and treatments than necessary. It’s like an all-you-can-treat buffet. You know you shouldn’t go back for that fourth General Tso’s X-Ray, but it’s just so delicious!

When all healthcare costs are covered, and the patient doesn’t need to pay regardless of how much he consumes, the patient is going to get more treatments and tests than he otherwise would. This increases the demand for healthcare, thus increasing the price, and as we discussed earlier, most of the price increases will happen to those who are privately insured.

Another reason for the high costs is the blizzard of paperwork generated by the interaction between dozens of insurers and thousands of providers. Both the insurer and the provider have to employ a team of unhappy people in cubicles to haggle over the reimbursement rate for an appendectomy. These teams add to the administrative costs of healthcare.

Simply put, the more distance you put between the patient and the health care provider, the more costly it will be. Health Insurance in general creates a lot of costly bureaucracy, and with almost two-thirds of healthcare covered by government, there is a lot of bureaucracy to go around.

The Affordable Care Act

Crash Course disappointed me in their analysis of the ACA and its effects on cost:

The Affordable Care Act also has provisions meant to deal with costs. And that’s a little more difficult to assess. The act rewards doctors for cutting costs, and requires greater price transparency. It also mandates a move to electronic record-keeping.

That’s the end of their comment on costs. Was this episode recorded in 2010? Is there no comment on if the ACA has or has not cut the costs of health insurance or healthcare costs?

Sadly, Crash Course’s political bias shows through in their analysis of the Affordable Care Act. While they show did note the law’s effect on the number of people insured, they did not comment on its effect on costs.

Crash Course Going Forward

Adriene: So, that’s the American healthcare system, which is weird and expensive, and necessary. That’s also the end of our textbook economics episodes.

Jacob: And so I’m moving to Canada to write a textbook and enjoy some of that sweet, sweet, subsidized health care.

Adriene: And I’m going to stick around and talk about the economics of things like immigration, and social security, and happiness.

So it looks like the textbook section of Crash Course Economics has come to a close, and the show will now be focusing on more topic-specific or behavioral economics subjects, which are not as exciting from my point of view.

Will Crash Course Criticism close its doors? Find out next Thursday!

Okay, the answer is no. I’m in it until the end, even if the subjects are no so economics-y.

This is the episode you’ve long awaited for: the minimum wage. I’ve been excited for this one since episode #20, where Crash Course talked at length about the dangers of price floors, and ended with this:

The vast majority of economists consider price controls counter-productive. But there is one notable exception: minimum wage. The minimum wage is a really complex issue that we’re going to address in a future video.

And finally, here we are. Let’s see if Crash Course explains why the dangers of price floors do not apply to labor. Here we go:

Labor Markets

Crash Course’s does a fantastic job in explaining the labor market. The entire segment is spot on, from how wages are determined to how the demand for labor affects wages. There are also some great nuggets of wisdom:

Engineers are in high demand because they produce the products that many consumers want and their supply is limited because the training for these jobs is pretty difficult. Social workers and historians, aren’t paid as much, even though their work is important, because demand is relatively low and supply is relatively high. It’s not rocket science.

While the supply and demand of labor play a major role in determining wages, I wish Crash Course had included a reference to the marginal productivity of labor. In other words, the market creates a natural ceiling on hourly wages: the amount of revenue one employee can create per hour. If an additional employee at a Pretzel Shop can only create an additional $9 in revenue per hour, the employer cannot possibly hire him from $10 an hour.

The Debate on the Minimum Wage: Bargaining Power

The economists that support a minimum wage argue that real life labor markets aren’t as competitive or transparent as classical economists suggest. They believe that employers have the upper hand when it comes to negotiating wages and that individual workers lack bargaining power.

Let’s imagine this scenario as described: an employer has an opening for one job at the Pretzel Shop. There is a long line of applicants who want the job, which gives the employer the pick of the litter. It looks like the employer has the upper hand here, since he doesn’t have to think about what wage to offer the applicant in their negotiation, and there are a lot of applicants to choose from.

Now imagine if there weren’t a minimum wage. The employer would be under a lot more pressure to offer the appropriate wage for the employee’s approximate skill, and offer a wage that is higher than other potential employers in town. With more jobs available around at below-minimum-wage levels, employees have a lot more options for employment and a lot more in bargaining power when finding new employment.

The point here is that employers have a greater bargaining power because of the minimum wage, not in spite of it, so I don’t see why this argument favors having a minimum wage.

The Debate on the Minimum Wage: The Nuts and Bolts

If a grocery store wasn’t required to pay $7.25 an hour, and the grocery store was the only place hiring, they could likely squeeze individual employees to accepting lower than market value. In this interpretation, minimum wage isn’t interfering with competitive markets, as much as it’s correcting a market failure.

This is strange, because back in episode 21, Crash Course taught us that a market failure is when the free market does not produce some good on its own, so it must be implemented by government (they use the examples of national defense and schooling).

In this week’s episode, it appears that a market failure is just something that happens in a free market that you don’t like.

Whether or not a grocery store is the only place hiring (something that’s very unlikely) wages are still determined as they always are: applicants compete on the bases of price and value provided. If the grocery store is the only place hiring, why should the grocery store be punished because of it? What about the businesses that aren’t hiring anyone?

Crash Course is also very peculiar in their wording of the above paragraph: Employers “squeeze” individual employees, while governments “correct” market failures. It seems that Crash Course is trying very hard to avoid using the word “force,” and for obvious reasons. In reality, employers never force anyone to accept the job, regardless of the wage, while governments do force employers to pay employees the minimum wage or more.

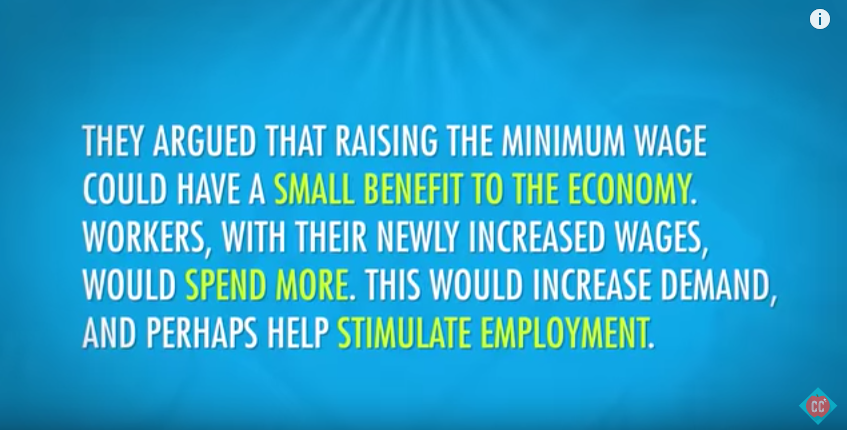

The Recently Developed Argument for The Minimum Wage

[Economists] argued that raising the minimum wage could have a small benefit to the economy. Workers, with their newly increased wages, would spend more. This would increase demand, and perhaps help stimulate employment.

This argument is a very popular one that I’ve only heard in the past few years. It sounds rather compelling, but it fails to account for a very important point of economics.

Crash Course did not flesh out this argument, but those who do argue it say that money, while in the hands of the employers/businesses, stays idle and doesn’t help the economy. On the other hand, if more money is given to the employees, the money is more likely to be spent and circulated, which is better for the economy.

Regular readers of Crash Course Criticism have heard me mention this in somanyposts, but saving and spending both play an important role in an economy. By artificially shifting the economy from saving to spending, the economy does not benefit or “create jobs” because of it. Money in savings is lent out by banks to entrepreneurs and small businesses, which also creates jobs. Shifting money from savings to spending would help create jobs in consumer goods (spending), but always at the expense of capital goods (savings), and the economy is no better off because of it.

Crash Course Neutrality

Crash Course has been surprisingly free market on some issues, and more pro-government intervention in other parts. This episode, unfortunately, very clearly supports having or increasing the minimum wage.

In the episode, before explaining the reasoning of both sides of the debate, Adriene quotes research from the Brookings Institute, a left-leaning think tank that supports raising the minimum wage:

The Brookings Institution estimates that an increase in the minimum wage likely wouldn’t just impact that small slice of the labor market. It would also drive up the wages of people who make just above the minimum wage. According to Brookings, that ripple effect could raise the wages of nearly 30% of the workforce.

Right off the bat, Crash Course is asserting that raising the minimum wage would raise the wages of 37 million working Americans. No negative effects mentioned, and certainly not a competing quote from a classical economist that would cite how many Americans could face unemployment because of the rise in the minimum wage. And when Crash Course eventually does summarize the classical economists view, they introduce it with “their logic goes something like this…“, phrasing it so that the audience knows that this theory is not well-reasoned logic.

Another annoying phrasing occurs right after Crash Course has summarized both sides:

I’m not going to tell you what to think, but think about it like this…

In other words, “I’m not going to tell you which theory is correct, but the following theory is correct…”

Wrapping Up The Episode

Crash Course finishes with citing some carefully-selected studies on the minimum wage, including a widely-discredited study in New Jersey:

If economics was a pure science, we could just test these ideas under controlled circumstances. We could have one state set a significantly higher minimum wage than its neighbor and see what happens. It turns out that happened in 1992, and economists David Card and Alan Krueger studied it.

First of all, since Crash Course taught us in episode 14 that Economics is not a pure science, they should know that a number of factors are at play for any employer anywhere at any time. Even if you look at two businesses across the river from each other, they are each subjected to infinite factors that could play into each business’s employment and wage decisions.

Additionally, Crash Course selects the one minimum wage study that has received the most negative criticism to my knowledge for its use of seriously flawed employment data. If you look into how the study was conducted, it is really astounding that this study was published after peer-review.

Crash Course started off the episode great with their discussion of labor markets, but the episode really took a turn for the worst when discussing minimum wage. Far from a balanced look at the minimum wage debate, Crash Course had its political bias out in full force. Despite its promise in episode 20, Crash Course did not explain why the economic laws of price floors do not apply to labor, and they did not attempt to rebut classical economist arguments.

But then again, if they did everything an Economics Crash Course should do, then we wouldn’t have Crash Course Criticism!

Thanks for reading, and you can look forward to a new episode reviewed every Thursday! And don’t forget to join our newsletter and our facebook group, and comment below!

This week on Crash Course Economics was not so much…economics. In this economist’s view, behavioral economics is more akin to psychology or sociology, despite having the “economics” in the name. Nonetheless, we are going to talk about some of the points that Crash Course did make on economics in this weeks episode.

The Big Picture: Predicting Behavior

When economists make their models, they generally assume that people are rational and predictable. But when we look at actual human beings, it turns out that people are impulsive, shortsighted, and, a lot of times, just plain irrational.

People often point to the existence of human irrational behavior to argue against economic truths that they might not like. For example, if you are arguing through economic logic that price controls make an economy worse off, a position that economists from all sides of the spectrum agree with, you might hear a response like “well, that assumes that people are acting rationally in their own self-interest, or with perfect information, but that isn’t always the case.”

While this might be true (there isn’t always perfect information, and people aren’t always rational) it doesn’t disprove any economic theories. What it does support, however, is that economics is very difficult to predict empirically. Let’s look at an example from this week’s episode:

Some grocery stores in the Washington DC tried to decrease the use of disposable plastic bags by offering five cent bonuses if customers brought reusable bags. The policy didn’t do that much. Later they tried a five-cent tax on plastic bags, and, this time, people used fewer disposable bags.

While empirical economists would be wrong in their predictions of the effects of the bag bonuses, those economists who shy away from empirical predictions (namely from the Austrian School) would only predict that there would be fewer plastic bags used than before, which is likely true.

In short, Crash Course’s big picture look at behavioral economics shows us how all those brilliant economists working for different government agencies and universities manage to get things wrong. The problem is not the theory, but the empiricism.

Lack of Information

Classical economics assumes that consumers have perfect information when making choices. That is, they know or at least can quickly access information about prices and quality, but, in reality, they often don’t. Sure, the consumer could ask around or call their friends to see if they’ve tried that type of ice cream but they’re probably not gonna do that. In this situation, consumers may act on the limited information they have, a suspiciously low price, which means either the ice cream is a great deal or it tastes like mayonnaise.

The way markets work is that the supply, demand, and price work out over time. Consumers might be cautious to any product at first, but as more people try the product and share the information about it (whether it’s on cnet, yelp, or amazon), the market tends to work itself out, even when it’s a little rocky at first. As Crash Course points out correctly, perfect information doesn’t happen all at once, but the market does move toward perfection as time goes on. As for the ice cream example, if the ice cream had a suspiciously low price but tasted like high quality ice cream, over time demand would meet the market’s expectations, although it might not happen at first. Ever heard of two buck chuck?

Nudging

Crash Course talked about a fantastic and recent theory in behavioral economics called Nudge Theory. Best explained in the book Nudge: Improving Decisions about Health, Wealth, and Happiness, Nudge Theory recommends an opt-out system of public policymaking, where the preferred choice is made easier or more visible to to the consumer, while still allowing the consumer to choose the less desired choice:

[Behavioral Economists] wanted to see if they could get children to eat healthier by rearranging school cafeterias. They put healthier food like fruits and vegetables on eye-level shelves and less healthy foods, like desserts, in less convenient places. Classical economic theory suggests that this idea wouldn’t work since rational people would pick the brownie. But it turns out, students choose the healthier foods. Nudge theory works and it’s changing how we implement public policy.

What Crash Course failed to mention, however, is that policymakers choose to impelement Nudge theory because it is particularly libertarian. If schools really wanted kids to stop eating unhealthy foods, they could just ban them entirely. Instead, Nudge Theory retain’s the consumers’ freedom to choose, while still encouraging them to make the healthy choice.

Bubbles are Caused by Animal Spirits?

Many economists used to believe that assets, like stocks and real estate, would stay at or near their real value because cold, calculating investors would buy undervalued assets and sell overvalued assets. But that doesn’t explain bubbles: In real life, investors aren’t always cold and calculating. They can get worked up and irrational sometimes.

This helps explain bubbles. From the Dutch Tulip Mania of the 17th century, to the 2008 financial crisis. Investors became irrationally exuberant, and were driven not by logic, but by what economist John Maynard Keynes once called, “Animal Spirits.”

This is very strange, since back in episode 7 on bubbles and episode 12 on the 2008 financial crisis, Crash Course explained bubbles quite differently. Back then, bubbles were created by complex financial products and lack of regulation, but maybe those were only the environments to create the bubble, and it was actually the animal spirits that created the bubble all along.

If you, as an economist, are going to stop your analysis of bubbles at “animal spirits,” you might be doing your audience an injustice. People blame a lot of different things for creating the 2008 bubble (legal incentives to encourage bad lending, poor credit-rating by agencies, monetary policy), but you can’t just dust off your hands and say “it just happens” Bubbles of 2008’s magnitude don’t happen with animal spirits alone. The spirits might do the popping, but bubbles are created by other factors.

Thanks for reading, and you can look forward to a new episode reviewed every Thursday! And don’t forget to join our newsletter and our facebook group, and comment below!