If you’re a regular reader of this blog, you saw the title of the thirteenth episode and thought it was too good to be true. Economic Schools of Thought? This might be the most important episode yet!

Personally, I think it was, as it does put the entire Crash Course series into perspective. I was really impressed with this video, so I’m going to start with the good things first:

Feathers in Your Cap, Crash Course

You do care!

First, it appears that Crash Course reads the comments section of youtube, something I’ve advised against doing in general, but it’s nice to see that Crash Course cares about its fans and what they want to learn about. Can you imagine if public schools were like this?

People are Often Wrong

Crash Course mentioned how all popular theories in science could be proven wrong.:

In 1798 British Economist Thomas Malthus argued that population growth will outpace food production, so eventually humans will run out of food […] Malthus was wrong, dismally wrong.

Economic theories are constantly being proven, disproven, and revised. The problem is , when these theories are wrong, millions of people can be adversely affected.

Here is where Crash Course could have thrown in how Malthus’s theory inspired some rather terrible political policies (eugenics). I don’t think the numbers were in the millions, though.

Again, Economics is not a Physical Science

Economics is not an exact science. It aims to draw conclusions about human behavior without the benefits of labs or perfect control groups. Economic theories reflect different attitudes about human nature, and those are likely to change over time.

Crash Course then goes through a the history of theories, includingCommunism and the Austrian School.

A Couple Critiques

I couldn’t let this episode go without pointing out a few (only a few though!) problems I had with the things said in the video.

The Great Depression crashed the market economies of the world’s richest countries. It also dealt a devastating blow to classical economics.

This is true; however, something needs to be said about Monetary Policy here. Certainly many people saw the Great Depression as evidence that the market doesn’t work, later schools of thought (The Austrian School and to a great extent, the Chicago School) explain the Great Depression was caused by increased government intervention into monetary policy.

Communists would probably say the same thing when Crash Course mentions how Communism failed. They would likely argue that it wasn’t communism that failed, it was just that these regimes didn’t implement it the right way (although I admit I’m less familiar with these arguments so I might not do them justice).

The Austrian School today argues that the economy is just too complicated to manipulate.

That sort of summarizes it, I suppose. I would say that the Austrian School argues that any artificial manipulations to the market (including the interest rate) create a less efficient economy that does not meet consumer needs as well as an economy free from intervention. Crash Course’s definition makes it seem like Austrians are economic agnostics.

Overall, this Crash Course video was fantastic. It introduced and explained (however briefly) different schools of economic thought, and more or less admitted that Crash Course teaches a specific school of thought, which combines Keynesianism and Classical Economics into something called New Neoclassical Synthesis. It’s almost like Crash Course admits that these videos are just, like, their opinion .

Crash Course’s most recent video on Fiscal Policy and Stimulus has its ups and downs. The show’s hosts acknowledge the controversy surrounding Keynesian economics, but not before treating the ideas favorably. The show equates free market economics with antiquated (and wrong) medical science, and presents only two (both government-centered) economic policies as the potential solutions to national recessions. Let’s start from the beginning:

Recessions vs. Unemployment

Crash Course spends the first few minutes of the video talking about what it means when a country is in a recession, followed by a brief history of recessions in post-WWII United States.

The episode notes that dips in the economy correspond with rising unemployment, and unemployment is linked to a number of other negative societal factors: namely suicide, domestic violence, and social upheaval.

Fortunately, Crash Course also mentions that unemployment is not the only potential monster to the economy. The show gives equal time to discussing the problems with inflation:

High inflation can be just as bad. Rising costs wipe out savings and have been the root of protests and riots around the world…

…Many economists argue that policymakers should intervene in the macroeconomy in order to promote full-employment or reduce inflation.

Without directly saying so (at least not yet), the show implies that large-scale unemployment and inflation happen naturally, and government policy may be necessary to fix these problems.

As I wrote about in last week’s episode on inflation, inflation doesn’t just happen naturally in the market. Widespread price increases happen from new money being created and flowing through the economy. When Crash Course says “many economists argue that policymakers should intervene in the macroeconomy,” they should also clarify that government monetary intervention has already occurred, and now people are considering if fiscal economic intervention is necessary.

To give them credit however, they are correct that unemployment would still occur in a free market. All schools of economic thought would agree that as industries are constantly growing and shrinking, and people get laid off when their industry shrinks. The real question between schools of thought is how a very high unemployment rate occurs, and whether government intervention prevents this from occurring (or causes it to occur).

Expansionary/Contractionary Policy

Before mentioning that what they are about to explain is debated between schools of economic thought, Crash Course explains Keynesian fiscal policy as generally agreed upon by economists. They later use examples from the 2008 recession to illustrate how this method of thinking is practiced in the United States, explaining away common objections to their example:

In 2009 the US government launched a huge stimulus program in response to the financial crisis. Despite that, employment and GDP both fell. That sounds like a failure, but the majority of economists think that the situation would have been far far worse without that stimulus.

I mentioned this in a previous post, but if a scientist declares his hypothesis to be true, and then despite their own contrary experimental results, still declares his hypothesis to be true, there’s no use trying to convince him. They will declare themselves the winner regardless.

Keynesian fiscal theory is based on two main assumptions: decreasing taxes and increasing government spending help the economy (and the reverse hurts the economy). Their own admitted problem is that helping the economy in this way requires the government to increase their debt, which will be paid back in better economic times.

Taxes hurt the economy. This is agreed upon by all economic schools of thought, even the communists. When you take away wealth from a people, what is left is worse off than before.

Government spending helps the economy. Freemarketeers may disagree with me here, but hear me out: government spending, per se, generally helps the economy. The problem is that government spending necessitates taxes in one form or another. Free market theory argues that money is better spent in the market than by governments, not that government spending (again, per se), doesn’t do anything good for anyone.

The problem is, you can’t have government spending without taxes, and while Keynesian expansionary policy may seem like you can have your cake and eat it too, issuing debt in the present is the same as taxing the future. Keynesian economic policy taxes the future for government spending and lower taxes in the present.

Since the increase in present government spending has to come from somewhere, this policy shifts spending from the future market to the current government. Since freemarketeers argue that any shift from the market (present or future) to government necessarily makes the economy worse off, freemarketeers oppose Keynesian fiscal policy.

So what’s up with the video’s comments on Austerity and the Multiplier Effect? Stay tuned for Part 2.

Like what I wrote? Hate it? Drop your feedback in the comments.

Economies grow and recede. Recently, people have related economic recessions to bursting bubbles. In 2001, the United States saw the Dot Com bubble burst, and in 2008, there we saw the housing bubble burst. The ebbs and flows have been a part of every economy since people started keeping track of economic data. But why does this happen?

Depending on which economic school of thought you prefer, you can have many different answers. Communists might argue that recessions are caused by capitalists acting in their own self-interest and taking advantage of the working class. For example, in 2008, banks were giving loans to people who could not afford to pay them back. When people stopped paying the loans back, money that was relied on was not there, and the economy suffered.

While this explanation of recessions (which can be summed up in one word: greed), is a catch-all for an incredibly complex economic dynamic that occurred over several years, it is not adequate. A real look into the business cycle would explain not just how the past recession occurred, but why recessions will continue in the future.

Crash Course and Keynesianism

We mentioned before how Crash Course, while admitting that there are different theories for economic phenomena, favors one in particular for macroeconomics: Keynesianism.

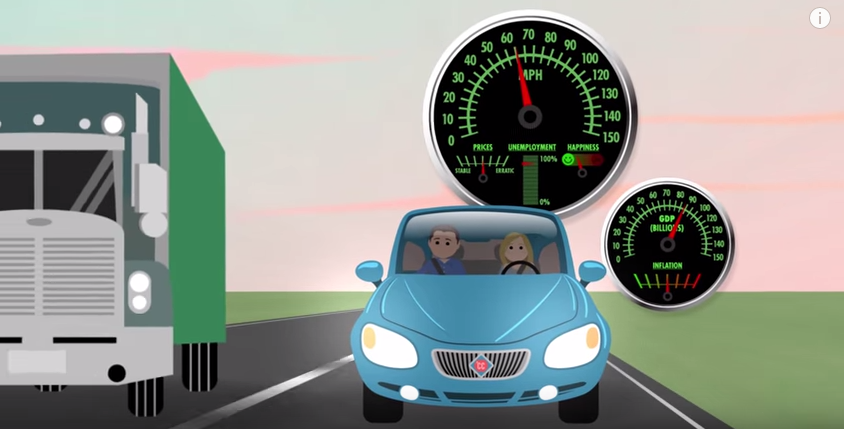

To be fair, the Keynesian explanation of the business cycle is also what is taught in your average economic textbook, so we shouldn’t be too surprised. It is explained in the video using the common analogy of a car:

If we imagine the economy as a car, then GDP, employment, and inflation are gauges. A car can cruise along at 65 miles per hour without overheating. Safe cruising speed is like full employment; unemployment is low, prices are stable, and people are happy.

But if we drive that car too fast for too long, it’ll overheat. In an economy significant spending increases GDP, causing an expansion. Unemployment falls and factories start producing at full capacity to keep up with demand.

Since the amount of products that can be produced is limited, people start to outbid each other, resulting in inflation. Eventually, production costs increase as workers demand higher wages and the economy starts to slow down. Businesses lay off a few workers. Those workers spend less, causing the businesses that produce the goods that they would otherwise buying to lay off more workers.

This is a contraction. The economy is going too slow. Eventually things stabilize, production costs fall as resources are sitting idle, and the economy starts to expand again. This process of booms and busts is called the business cycle.

A lot of this explanation is fluff, but the essential explanation of the business cycle can be cut down to the following:

People start to outbid each other [for resources], resulting in inflation. Eventually, production costs increase as workers demand higher wages and the economy starts to slow down.

Essentially, the price of raw materials increases, and workers demand higher wages. The combination of the two hurts business, which starts the downturn. Let’s take a look at these two separately:

1. Increase in the Price of Raw Materials

Resources are scarce, and businesses have to compete for these resources. When businesses are doing well and demand more of these scarce resources, the price must increase, since the supply cannot increase. The increased price weakens the businesses.

But businesses can also forecast the prices of raw materials. In fact, many businesses hire people to do exactly that. Rising prices like these should come as no surprise to businesses, and if they are expected, they would be accounted for in a way that minimizes damage to the business.

Additionally, rising prices in the provision of raw materials would signal to the market that more resources need to be devoted to it. The raw materials business is booming in this scenario, so the industry would be hiring workers as the demand for their resources increases. The market would be shifting jobs from one area of the economy to another, which is normal. I don’t see how unemployment results from this.

2. Workers Demand Higher Wages

This is a huge assumption: over time, workers demand higher wages, so employers choose to increase wages, and have to lay off some workers as a result.

This just doesn’t happen. An employer will usually do what’s good for the business, and if it’s a large company with shareholders, the owner has a fiduciary duty to do what’s good for the business. In other words, if the CEO of a company knowingly does something that will hurt the business, he/she gets sued.

Sometimes, employees are paid less than what the employer would pay, and the demand for higher wages results in higher wages. This often happens in a boom economy: employees have many job options, forcing employers to pay them more to keep them at their current job. But if the employer cannotafford to give higher wages (and we know this because increasing wages would result in lay offs), he won’t, and in many cases, he legally cannot.

Wages are determined by the amount of value created, how much the employer is willing to pay, and how much the worker is willing to work for. The worker’s demands alone does not determine his/her pay, and businesses likely will not weaken themselves because the employees ask it.

3. The Spending Spiral Takes Care of the Rest

While the cause of the downturn is debatable, Crash Course’s explanation of the result is rather accurate. Once businesses start losing money, they start laying off workers, who spend less in the economy, so everybody hurts.

Please note that this is a different situation from that my last post, where money is shifted from spending to saving. In the current case, spending and saving is replaced with nothing.

The Role of Government

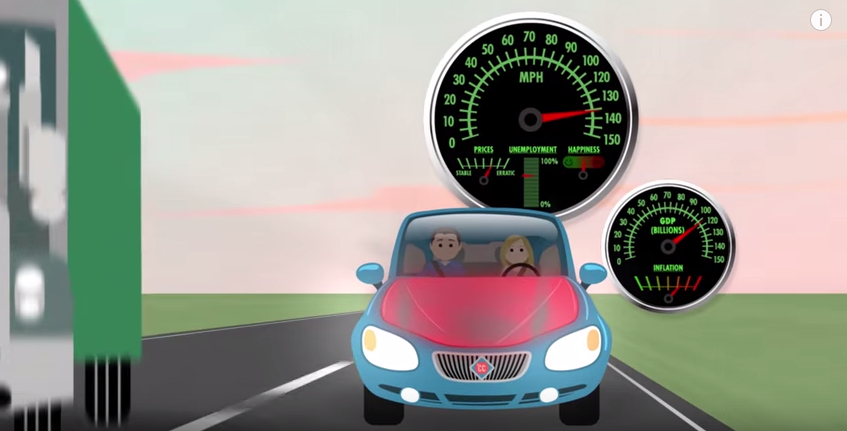

According to Crash Course (and many economics textbooks), the above explanation is what naturally happens in a free market economy, and economists generally favor the government to step in to fix it (again using the car analogy):

When I’m driving my car on the highway I like to use cruise control to regulate my speed. So why don’t we have cruise control for the economy? Well, many economists think that the government should play a role in speeding up or slowing down the economy. For example, when there’s a recession, the government can increase spending or cut taxes so consumers have more money to spend.

Proponents of this policy argue that it would get the economy back to full employment, but it has its drawback: debt.

Increasing spending or decreasing taxes (absent other changes) would increase the debt, which Crash Course will get into in another video.

My problem is the assumption that government must have nothing to do with the cause of the recession; it is only shown as the possible solution.

Crash Course Criticism will get into alternative business cycle theories and the other possible causes of recessions when we get to the videos on the Federal Reserve. We have a lot to talk about here. Stay tuned.

Like what I wrote? Hate it? Drop some feedback in the comments.

John Maynard Keynes is probably the most influential economist in currently-practiced economic policy. Among the Keynesian marks left on economics is the idea of the necessity of government intervention to moderate the booms and busts of the economy. As the theory goes, governments must spend during a recession to stimulate the economy.

This idea makes a lot of sense if you’re hearing it for the first time. When you’re tired, coffee helps you get back to normal, and similarly, if the economy is down, you need to kickstart it with some spending to get the ball rolling again.

Adriene alludes to this idea when she says:

Economics is the government deciding whether to increase its spending when there’s a recession, and if it’s worth going into debt.

Usually the answer is yes, increase spending, as the United States did with its $831 billion Stimulus Package (also known as the American Recovery and Reinvestment Act of 2009).

The problem with testing economic theories is that you never know if it actually works. The 2009 Stimulus Package did not have the kickstarting effect that was predicted; the free-market economists said that this was because Keynes’s theory is wrong and government spending does not help the economy because a stimulus package would only take money from the more efficient private sector economy (through taxation) and transfer it to a less productive public sector economy. However, Keynes supporters argue that Keynes is correct and the Stimulus Package did work, and the situation would have been much worse if the government had not intervened.

Unfortunately, we’ll never know the truth empirically, since economics is not a physical science where you can have an identical “control group” economy to compare it to. And while Adriene’s point didn’t directly claim Keynes’s theory to be true, she did imply it. By presenting the downside of spending as “going into debt,” which isn’t necessarily true, she doesn’t mention what real dissenters of stimulus spending would argue: that stimulus packages are a net negative for the economy, even if the country doesn’t have to borrow money to pay for it.

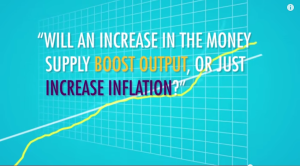

Mr. Clifford makes another Keynesian presupposition when he posits this question as an example of macroeconomics:

Will an increase in the money supply boost output, or just increase inflation?

Framing the question this way essentially presupposes that increasing the money supply can boost output, but the risk is that it mayalso increase inflation.

This is also derived from Keynes’s theory of government intervention for a recessed economy: increasing the money supply (i.e. creating money and buying financial products with them) will give more money to banks who then lend out that money to people for long-term capital projects (building construction, investing in companies, etc.). Now there’s more money circulating in the economy as more people get to borrow money to fund their projects, and the financial industry is booming because they are the first ones to get the newly-printed money. However, printing money runs the risk of prices increasing as the dollar becomes less valuable. The Keynesian theory describes money creation as a balancing act; the government needs to print just enough to kickstart the economy, but not too much to create an inflation problem.

Again, real dissenters from Keynesian economic theory (or at least those who follow the Austrian Business Cycle) would argue that increased inflation is not the only risk of increasing the money supply. As the Austrian theory goes, money printing distorts the economy, shifting production from consumer goods (like stuff you buy at CVS) to capital goods (projects that banks give big loans to). The shift is harmless at first and may even appear to boost the economy, however, this distortion that provokes an artificial boom will ultimately result in an even greater bust. In other words, the cups of coffee you drank to wake you up will leave you with a bigger caffeine withdrawal the next day.

With these two examples, it’s not too hard to see a preference toward Keynesian macroeconomics, but who can blame them? Keynesianism is widely-practiced in countries around the world and is supported by many economists.

The least they can do, however, is correctly present the real concerns about Keynesian policies, and not the Keynesian concerns about Keynesian policies.